When you buy a warehouse, a strip mall, or a small apartment building, you are largely buying the leases.

You underwrite the rent roll. You look at the remaining lease terms, the credit of the tenants, the escalation clauses, and the probability of renewal. The income stream you are buying has contractual shape. If an anchor tenant has seven years left on a lease with a national credit guarantee, that tenant is effectively part of the asset itself.

Self-storage does not work this way, and buyers routinely underwrite it as if it does.

The average self-storage tenant stays roughly 18 months, and the distribution is heavily skewed. Most tenants churn within the first year or two, with a smaller long tail of tenants who stay much longer.

If you close on a property on July 1, 2026 with 200 tenants in place, within two years most of that rent roll has turned over. Within five years, even the long-tail tenants have largely cycled. The rent roll you closed on is not a durable asset; it is a snapshot of a constantly refreshing customer base.

This has real implications for how you underwrite:

The occupancy and achieved rates you see at close tell you how the facility has been performing recently. They do not tell you how it will perform under your ownership. Nearly every dollar of that rental income is going to need to be re-won within a couple of years.

If the seller has been aggressive with existing customer rate increases, a meaningful portion of current revenue is sitting on tenants who are already priced above street. Those tenants will turn over at street rates, and every month the gap between “achieved” and “street” narrows as turnover compounds. If you paid for revenue that was effectively borrowed from future rate compression, you overpaid.

In a warehouse deal, a new competitor next door doesn’t break your existing 7-year lease. In storage, a new competitor down the street can re-price your entire market within a couple of years because your tenant base rolls during that window.

You don’t have contractual protection — you have a physical asset competing in real time.

With certain assets and businesses, new supply and options are great. Vegas wouldn't be Vegas if there was only one hotel. Mall tenants actually suffer when anchor stores close, which is the opposite of what simple supply-and-demand would predict. Food courts, food halls, and restaurant rows are master planned by developers who pay to cluster these businesses together, because the agglomeration grows the pie for everyone in it.

Storage is not like this, at all. Nobody drives past three storage facilities to get to "the good one." There's no destination effect, no anchor tenant, no cluster that pulls new customers into a market. A new storage facility has essentially no benefit to an existing storage owner. It's pure redistribution of a fixed pool of local demand.

Here is a useful thought experiment. Imagine you are presented with the same facility twice (same building, same market, same competitive set, same unit mix). In one version, you take possession with the existing rent roll. In the other, you get the keys to an empty building and have to fill it up from zero.

Obviously your year-one and year-two cash flows look completely different. In the first version you are throwing off NOI from day one. In the second you are working through a fill-up period.

But by year five, it is the same physical asset in the same market under your operation. The stabilized NOI should be the same. There is no reason it wouldn’t be.

Which means the premium you should be willing to pay for the occupied version over the empty version equals exactly one thing: the NPV of the fill-up head start. Not more. If you are paying more than that, you are paying for an income stream you don’t actually own. Instead, you’re paying for the seller’s operating history, which does not transfer to you.

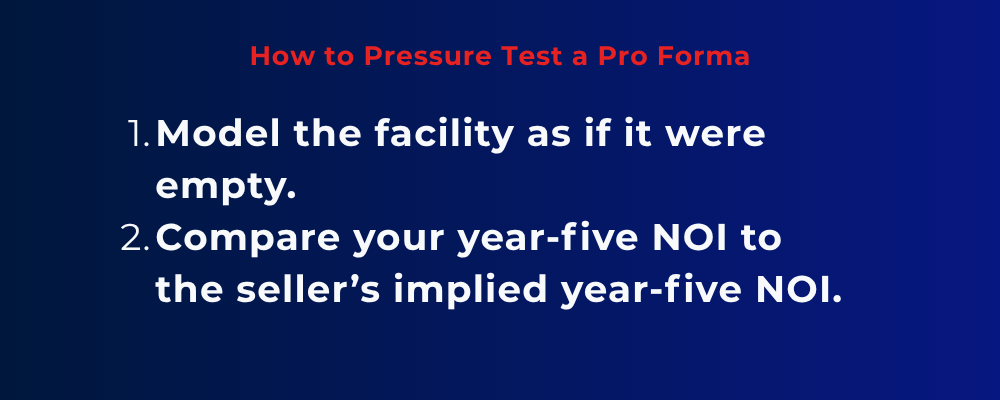

This is the cleanest way to pressure-test an acquisition pro forma. Strip out the acquired rent roll entirely and model the facility as if it were delivered to you empty. Your year-five NOI should match the seller’s implied year-five NOI. If it doesn’t, one of your assumptions is wrong, and it’s probably not the empty-building version.

If you’re not buying the rent roll, and the seller’s operating history doesn’t transfer to you, what’s left? Really two things:

1. You are buying the supply and demand dynamics of a specific local market.

2. And you are buying a physical asset, a building on a piece of land, in a specific location, with a specific unit mix and condition.

Your operating platform matters enormously, but it isn’t something the seller can sell you. It’s the thing you bring to the deal, and it determines whether you can actually realize the NOI the market and the building make possible.

Those are the inputs that will determine what your rent roll looks like two years from now. In the next piece I’ll dig into each one and the big questions you should be able to answer about them before you close.

The discipline in storage acquisitions isn’t underwriting the rent roll you’re buying. It’s underwriting your ability to rebuild it.